Wall Street has not turned its back on climate change

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

In January 2025 the Net Zero Asset Managers (NZAM) initiative, the flagship coalition setup in 2020 to align the asset management industry with global climate goals, announced that it was suspending its activities. Days earlier, the worlds largest investor group, BlackRock, said that it was leaving the group amid a political backlash in the United States.

Other coalitions of financial institutions, such as the Net Zero Banking Alliance (NZBA), setup to provide guidance to banks on setting climate goals, have also quietly loosened their climate ambitions. In part the move recognises that the world is not now very unlikely to meet the 1.5°C target, but also reflects escalating energy security concerns.

The NZAM, NZBA and other similar initiatives were underpinned by mandates requiring signatories to measure, disclose, and report on climate related information.

However, it's clear now that the assumption that simply by adopting "climate risk" mandates financial institutions would go onto allocate capital in such a way that we would avoid planetary breakdown, was a mistake.

That's the main conclusion from a new paper from the Columbia Center on Sustainable Investment (CCSI).

Rather than accelerate action to tackle the climate, the mandates have only served to slow the transition, meanwhile stoking discontent among climate activists, and emboldening climate deniers and delayists.

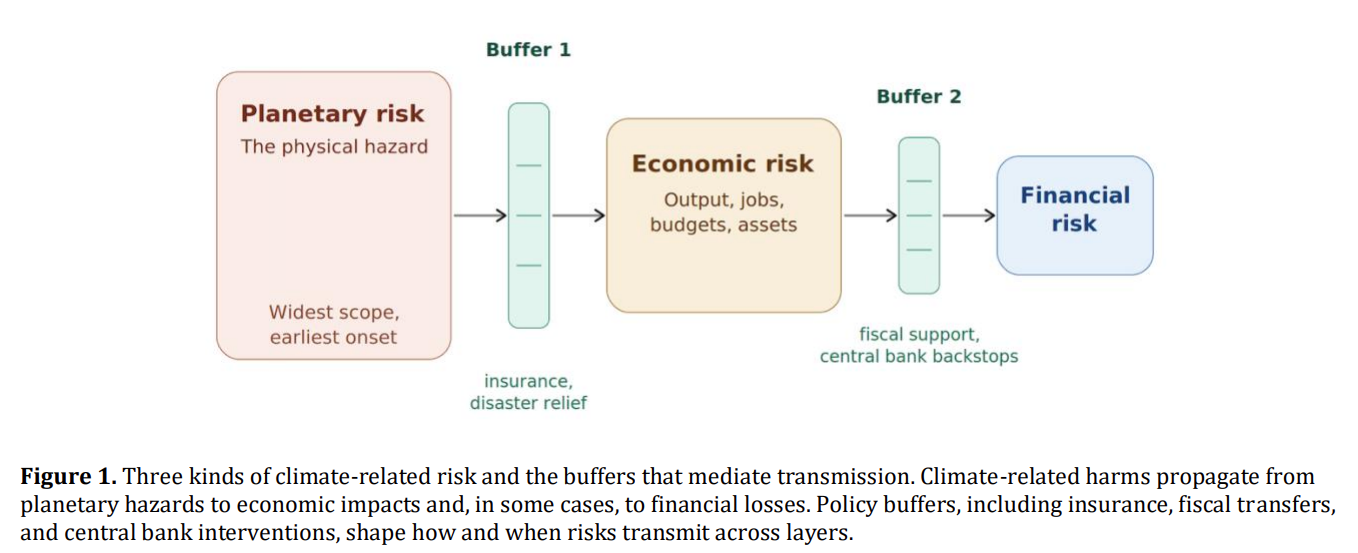

The key problem identified by the CCSI is that "climate risk" conflates three distinct types of risk:

- planetary risk - rising temperatures, sea level rises and the human and ecological harm they cause.

- economic risk - physical and transition risks that affect incomes, infrastructure, and public budgets.

- financial risk - impact on credit quality, portfolio values, and risks to financial system stability.

Climate change gives rise "not to a single undifferentiated 'climate risk', the report argues, but to a "cascade of interconnected yet distinct risks." As the image below illustrates, the risk propagates from left to right, from planetary risk to economic risk, before finally manifesting in financial risk.

However, as the CCSI make clear, mandates have loaded institutions with expectations that are "misaligned with their mandates and tools, and undermines the tools and focus they do need to manage the risks they actually face."

Only emission mitigation tackles the underlying hazard posed by climate change.

The other five responses identified by the report - adaptation, risk sharing, fiscal resilience, exposure management, and financial system stability - manage the consequences of climate change downstream.

As the CCSI conclude, disentangling the three distinct risks is a "precondition for responding effectively". Instead of expecting institutional mandates to be a Swiss Army Knife, far better to match "each objective to the appropriate institutions and tools."

In January this year, twelve months on from the collapse of the NZBA, the New York Times published an article titled, "How Wall Street Turned Its Back on Climate Change: Six years after the financial industry pledged to use trillions to fight climate change and reshape finance, its efforts have largely collapsed."

In contrast to the negative headline, it's clear that financial institutions have adapted how they are responding to climate change. Far from abandoning climate change, institutions are using their influence to help shape public policy, prepare business owners and investors for the breadth of risks they will face, and in light of the current challenges affecting the world, fighting the complacency trap.

For example, this week 49 investment institutions, representing €13.1 trillion ($15.1) in assets under management, issued a joint letter urging Europe's Heads of State "to preserve the carbon market as a credible long-term investment signal." The letter says that the EU ETS must remain "the bedrock of Europe’s clean industrial future," adding that "the ETS revision presents an opportunity for evolution – not dilution."

As ever, what's most important to institutions, especially when allocating long-term capital to low-carbon technologies is stability. "For institutional investors", the letter goes onto say, "regulatory stability and visibility on the likely future carbon price path help manage risk and enable long-term capital deployment into the real economy."

Among the six recommendations the group calls for, the letter cites the need for clear and credible long-term cap trajectory aligned with Europe's long-term climate goals, transparent rules that provide a predictable upward price signal, and increased support to help industrial companies decarbonise while also addressing sectoral structural barriers to competitiveness (see EUAs reaching critical turning point: Despite the noise, EU ETS reform discussions are yet to start in earnest).

The need to accelerate mitigation is more important than ever. Europe is already suffering from climate change - heat stress events have multiplied sevenfold since the 1980's - and this year could be even more extreme as El Niño has officially begun. It's clear that climate change is

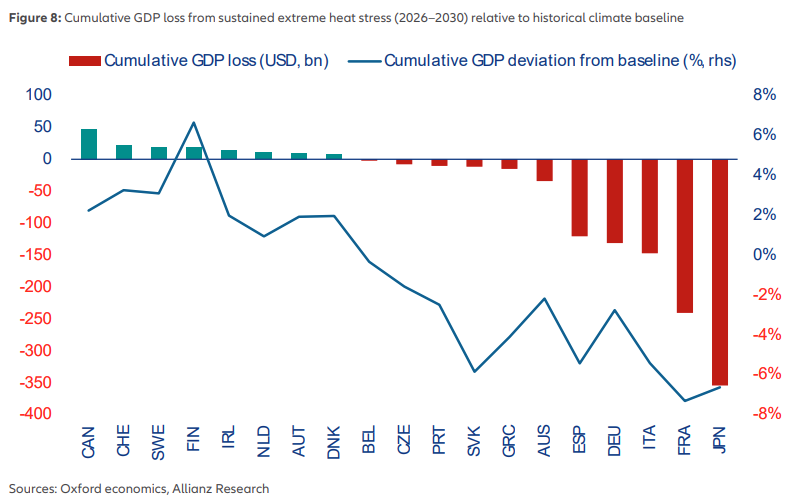

One of the signatories to the European Heads of State letter, Allianz SE, published a report in May arguing that extreme heat has now become a structural economic risk for the continent. They report that Europe is highly exposed to these ill-effects due to a combination of ageing populations, housing designed to retain warmth (rather than keep cool), and finally, low investment in cooling infrastructure such as air-conditioning.

A crucial insight from the report is that the economic losses from heat stress are non-linear; there is a critical threshold above 30°C beyond which the productivity losses intensify sharply. The losses fall most heavily on France, Germany, Italy and Spain, with one scenario pointing to cumulative implied GDP losses of 5-7% over the next four years.

Despite the pressing urgent need for investment in mitigation, L&G Asset Management (another of the signatories to EU letter) believe that many investors may have been led into believing the narrative that the energy transition has stalled, and that uncertainty over the climate means "long-term analysis has little merit." The asset manager believes that these two misunderstandings mean investors are now placing "too great a focus on short-term returns over long-term capital allocation to the energy transition."

However, holding back in committing capital to decarbonisation means companies could be exposed to significant risk, and mean missing out on capturing the opportunities from the energy transition. L&G also believe a "potential fear of first mover disadvantage and a hesitation to compete with Chinese dominance in many low-carbon technology markets" may be leading companies to hesitate before investing.

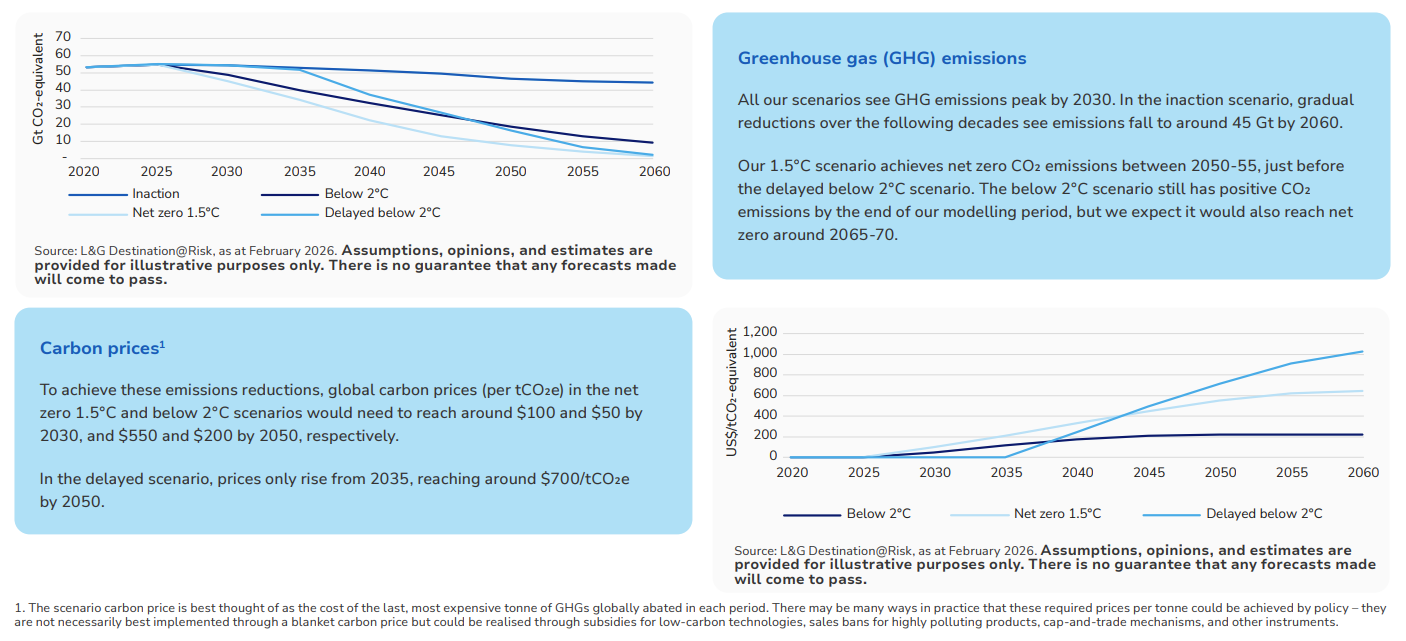

Updated scenarios prepared by the asset manager indicate that global emissions are likely to begin falling later this decade, even without further policy support. However, this alone will not be sufficient to keep global warming below 1.5°C or 2°C. To achieve the required emission reductions L&G estimate that carbon prices will need to rise to $100/$50 per tonne CO2e by 2030, increasing to $550/$200 per tonne CO2e by 2050, respectively.

Importantly, for investors (and the economy at large), there is the possibility of a disruptive pathway where climate policy suffers a decade of delay and disappointment. In this delayed scenario, carbon prices would only begin to rise from 2035, but would need to reach $700 per tonne CO2e by 2050 to meet the global warming targets. This would clearly involve much higher planetary, economic and financial risks, and do much greater damage.

As per the footnote there are many ways that an equivalent carbon price could be implemented, and not necessarily best implemented through a blanket carbon price. L&G include subsidies for low-carbon technologies, sales bans for highly polluting products, and cap-and-trade mechanisms on the list of potential policy instruments.

The term Tragedy of the Horizon was coined by former Governor of the Bank of England, Mark Carney. This is the idea that the catastrophic impacts of climate change will be felt beyond the traditional horizons of most actors. This imposes a cost on future generations that the current generation has no direct incentive to fix. In a speech to the finance industry at Lloyds of London in September 2015, Carney suggested that climate disclosures were the answer:

“With better information as a foundation, we can build a virtuous circle of better understanding of tomorrow’s risks, better pricing for investors, better decisions by policymakers, and a smoother transition to a lower-carbon economy.

By managing what gets measured, we can break the Tragedy of the Horizon.”

Better information is the foundation and while important, it's clear now that simply pursuing climate risk disclosure mandates was an insufficient condition for tackling the underlying issues. To reiterate a sentence from earlier, mandates loaded institutions with expectations that are "misaligned with their mandates and tools, and undermines the tools and focus they do need to manage the risks they actually face."

Progress would have bene faster if this had been identified sooner, but it's not all bad news. Far from it. It's clear that financial institutions are using their leverage to play a more active and crucially, a more targeted role in tacking underlying climate risks. In a subsequent post I'll explore how financial institutions are now tackling other 'non-mitigation' responses to climate change, including using the power of markets to change incentives.