Repost: California's 'energy transition' will not be linear

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

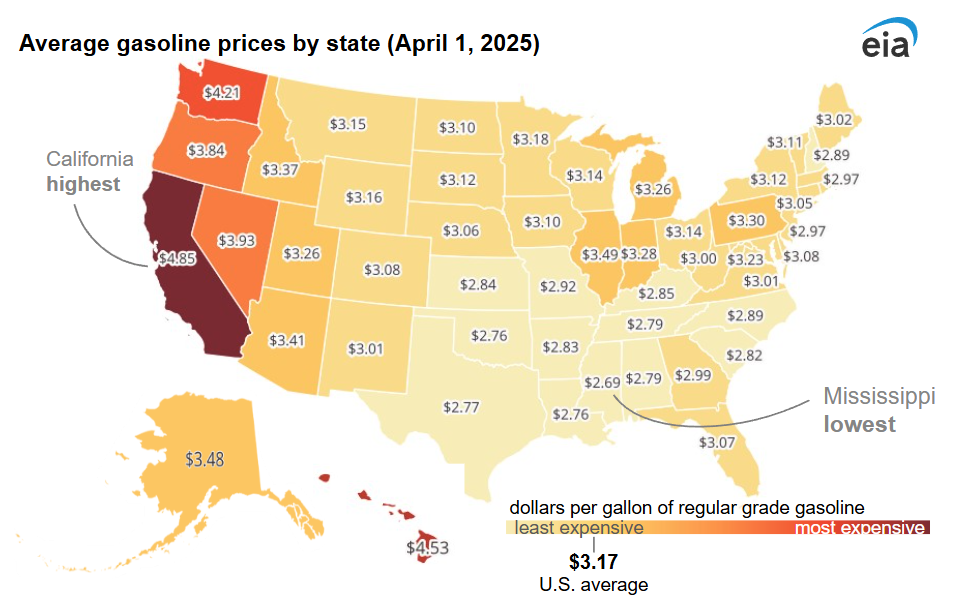

Gasoline prices in California have surged by around 30% since the start of the US-Israeli conflict with Iran, and now stand at more than $6 per gallon, almost 40% above the US national average.

In recent months California has become increasingly dependent on refined product imports after two of its largest refineries shutdown: the Phillips 66's Los Angeles and Valero's Benicia facilities.

What's made things worse is that South Korea, the states main supplier of jet fuel, is heavily dependent on crude supplies from the Middle East. The conflict in the Gulf has forced its government to cap refined product exports.

As I discuss in an article first published in May last year (and now available below without the paywall), California is discovering that it's 'energy transition' is anything but linear. Managing the decline in refining capacity is a delicate balancing act, which if handled badly risks a backlash against the states climate policies.

The gasoline price surge, coinciding with a contentious overhaul of the states 'Cap-and-Invest' market, could not have come at a worse time. High prices appear to have handed the states remaining refiners significant political and economic leverage.

But is the reality quite as clear cut?

Last week the California Air Resource Board (CARB) voted 10-3 to adopt revisions to the scheme that seek to balance ambitious emission reduction plans, with concerns over affordability and competitiveness.

At the centre of the controversy lies the Manufacturing Decarbonisation Incentive (MDI).

As outlined in an earlier article, the MDI will provide additional free allowances (118.3 million) to facilities if they invest in certain emission reduction activities. About half of the allowances are available to be used by the states refiners, a sum that could be worth close to $2 billion.

The worry according to a recently published analysis of the MDI is that refineries may end up with more free allowances than they need to cover their emissions. Although CARB has now built in review periods after each compliance period, its still unclear how they will determine whether a refinery has invested in emission reduction activities such that they will be allocated free allowances.

Its good news that this present bout of policy uncertainty is now behind us. Hopefully it means that the price of allowances can now begin to lift themselves off the floor. Encouragingly, the CCA futures price closed near $30 on Friday, the first time it has moved away from the auction reserve price since February.

Whether that is a vote of confidence in the amendments or not, it's too early to say. The increase in the carbon price perhaps reflects scepticism that refiners will ever be in a position to qualify for the additional allowances under the MDI anyway.

Two major refineries in California have announced plans to close over the next twelve months. The Phillips 66 refinery in Los Angeles is scheduled to shut-down by the end of 2025, followed by the Valero refinery in Benicia in April 2026.

The shutdowns should curb emissions by around 3 Mt of CO2e. After power generation, the refining sector is California’s second largest emitter — it’s top five individual emitters are all oil refineries.

However, the two facilities slated for closure also produce approximately 20% of California’s in-state gasoline supply, raising fears about whether the state will have enough gasoline to ward off the threat of a price spike. Indeed, analysis by Professor Michael Mische of University of Southern California (USC) forecasts that gasoline prices could rise to above $8 per gallon by the end of 2026, if the refining supply crunch is allowed to manifest.

Mische’s analysis indicates that the price of gasoline could rise from around $4.85 per gallon currently, to between $6.05 and $6.43 per gallon following the closure of the first refinery, increasing yet further to between $7.35 and $8.44 per gallon by the end of 2026 as the second refinery closes.

Even if the exact gasoline price trajectory is someway short of these predictions, sharply higher fuel prices risk provoking a backlash from citizens. Up until now at least they have been somewhat shielded from the supply-side response to California’s environmental policies.

That looks set to change.

An “energy island”

It’s no secret that Californian’s face the most expensive gasoline prices in America, with drivers typically paying around at least $1 more per gallon than the national average, and often more than $2 per gallon higher. Other western states also see high gasoline prices, but not to the extent to that experienced in California.

In part this is because the region is so geographically isolated. The vast Rocky Mountain range to the east means that there are no pipelines able to deliver gasoline directly from the US Gulf and other refining centres. Instead, California often has to import gasoline across the Pacific, from countries such as India and South Korea, in order to make up any shortfall, which of course adds to the overall cost.

The high price of gasoline also reflects a political choice, one that has been influenced by California’s history as being among the worst states in America for air pollution. The topography of the state means that noxious fumes become trapped, often resulting in a thick smog enveloping the cities below. As the most populous US state, transportation has played a central role in driving air pollution; the sector is responsible for 80% of the states nitrogen oxide and 95% of its particulate matter emissions.

In response, California mandates a special blend of gasoline (known as California Reformulated Gasoline), that burns cleaner than conventional gasoline, reducing air pollution and greenhouse gas emissions. The blend is more expensive to produce than conventional gasoline, and so California tends to rely on its in-state refineries to produce it.

Other factors also mean the state has become progressively less attractive to refiners. For example, the Low Carbon Fuel Standard (LCFS) has increased the incentive to produce renewable biodiesel rather than petroleum diesel. California has also tried to incentivise a switch towards zero emission vehicles (ZEV) via its mandate program (see Everything you need to know about Low Carbon Fuel Standards (LCFS)).

Blowback

As the state gradually winds down its gasoline consumption, energy companies face the real risk that their refineries may become “stranded assets”. It’s a policy choice and their closure is the natural end result. The problem now is how to best manage the transition away from gasoline to avoid consumers facing a nasty shock that turns public opinion.

One of the main issues facing California is its low level of gasoline storage. The state typically holds ~20 days of gasoline supply in inventory at any given time, making it vulnerable to adverse supply issues and the knock-on impact on gasoline prices. In the current environment there’s simply no incentive for refineries to invest in the type of storage facilities that could mitigate the impact of any gasoline shortage.

When refineries close down its usually good news for those facilities still operating as they are now able to benefit from higher margins. That might not be the case in the future, at least for California’s remaining refineries. In October 2024 Governor Newsom signed a controversial new law (ABx-21) giving the state sweeping powers to curb refineries ability to profit from shortages.

The mandate empowers the state to implement a profit margin penalty or price control on energy producers, to limit when refineries can conduct maintenance, requires refiners to stockpile large volumes of fuel, and increases state oversight of their operations. Although the law was meant to ensure adequate gasoline supplies, it has inadvertently made things worse. Both refineries due to close appear to have brought forward their announcement following the signing of ABx-21.

Cap and invest

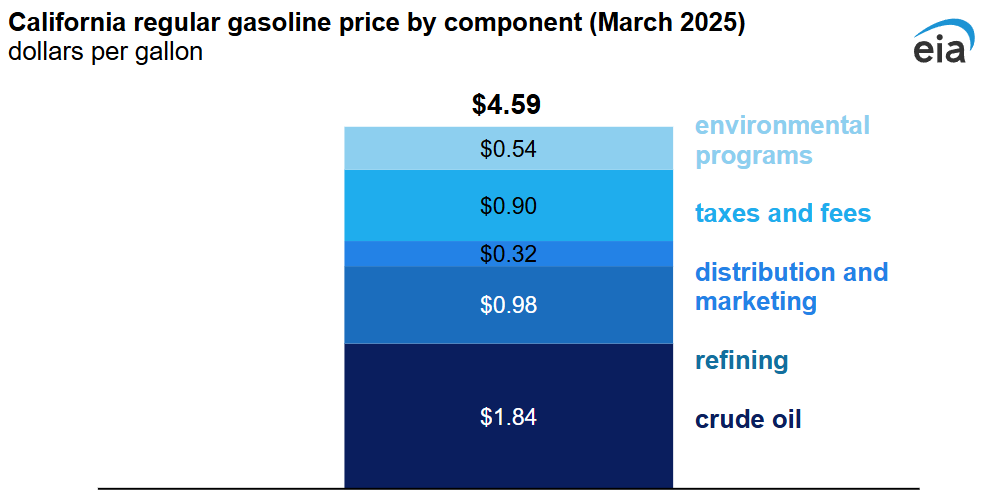

Although environmental programs such as California’s emissions trading scheme and the LCFS often get the blame, there’s no evidence that they contribute significantly to the overall cost of gasoline, despite their cost typically being passed on in full to the consumer. According to the California Energy Commission the programs accounted for $0.54 per gallon (~12%) of the retail gasoline price in March 2025, roughly split 50/50 between the carbon price and the cost of meeting the LCFS.

Carbon prices are low right now, but what happens if the market rebounds as is likely to happen if the scheme is reauthorised to continue post 2030? If the price rebounds from current levels close to the Auction Reserve Price ($25.87 per tonne of CO2) and returns levels seen last summer (~$40 per tonne of CO2), it is likely to increase gasoline prices by ~$0.24 per gallon. Although that doesn’t sound very much in the scheme of things, the pain of the increase becomes more acute to California’s drivers if it coincides with a period in which gasoline prices are very high because of other reasons — for example, due to a spate of refinery closures (see The future of California's cap-and-trade program beyond 2030 is now in doubt).

Very high gasoline prices should mean lower emissions as drivers scale back the number of miles they travel, and / or switch to more fuel efficient and lower carbon alternatives. In theory this means less demand for emission allowances (CCAs) and a lower carbon price. The problem is that retail demand for gasoline tends to be highly price inelastic – an increase in its price does very little, at least in the short-term, to curb demand. The impact of high gasoline prices also falls most heavily on those least able to adapt. For example, lower income households are less likely to be able to afford an electric vehicle.

What to do? As I note in America's state carbon markets are under siege, Governor Newsom faces a quandary:

“On the one hand he knows that California is likely to face huge and ongoing budgetary shortfalls — potentially more than $10 billion per year…On the other hand Newsom knows that if his policies are seen as being responsible for pushing up the price of gasoline and electricity in California, then his chances of becoming the Democratic nominee ahead of the 2028 presidential election are very slim indeed.”

The best response would be to reauthorise the carbon market, extending its remit beyond 2030. This would lead to higher CCA prices, resulting in higher revenues from the auction of allowances that could then be used to plug the states budget deficit. The state could then direct more funding to make it easier for citizens, especially those on lower incomes, to switch to lower carbon alternatives. Remember, evidence suggests that simply returning carbon revenue back to consumers is difficult to target effectively, it messes with the carbon price signal, it’s challenging to communicate, and most importantly, it fails to address switching barriers (see Why Canada should reform its carbon tax).

The energy transition was never going to be a straight-forward linear process. You need to factor in the disjointed nature of the supply-side response in a declining market. In the example of California, the strongest refineries will always try and stay in business for as long as they can, benefitting from higher margins as weaker ones leave the market. Eventually, firms decide enough is enough and they need to cut production or close up shop completely. More refineries will inevitably close as the state moves towards achieving its 2045 targets.

In the meantime California needs to do more to prepare its citizens for the non linear path ahead. Focus more on adapting demand, less on constraining supply.