Persistent UKA-EUA spread reveals deep political paralysis

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

Last week the UK government announced that the Carbon Pricing Scheme (CPS) is to be abolished from April 2028.

To recap, the CPS is an additional carbon price paid by fossil-fired power generators. Crucially, it's a top up tax, over and above what utilities pay under the UK ETS. It was launched in the early 2010s when carbon prices in the EU were below €10 per tonne CO2, coal accounted for about 40% of the UK's electricity generation, and the UK government (then led by the Conservative Party) were concerned that they would not be able to meet the targets outlined in the 2008 Climate Change Act.

The CPS was instrumental to securing coal's fate, dealing a fatal blow to coal plant economics. Launched in 2013 at £5 per tonne, it rose to £9 per tonne CO2 in 2014. Since 2015 it has been frozen at £18 per tonne CO2, equivalent to €20.70 today. For a while during the mid-2010s, UK generators paid more than four times the prevailing carbon price facing those located on the continent. Almost two years ago, Britain made coal history and closed its last coal-fired power station. The policy had down its job, and as so often happens (or at least should), its success ultimately brought about its demise.

The CPS hastened the decarbonisation of the UK electricity grid, but it had outstayed its welcome. The CPS accounts for around 8% of the short run marginal cost for gas-fired power generators, according to estimates by the Centre for British Progress. By driving up the wholesale price of electricity relative to natural gas it is now arguably delaying electrification in the UK.

Given that power generation is already under the UK ETS emissions cap (the cap is fixed and declines each year), the withdrawal of the CPS will not have any direct impact on covered emissions. As the Institute for Fiscal Studies (IFS) argues, while the lower price of electricity might induce higher demand for power generation, any resulting increase in emissions should be offset by lower emissions elsewhere within UK ETS covered sectors.

Outside of the realms of the UK ETS cap however, electricity prices should decline relative to natural gas and other fossil fuels, steering both households and businesses towards greater electrification. To the extent that electric transportation, heating, and other applications are significantly more energy efficient than their incumbent fossil-fuel alternatives, the loss of CPS could spur a decline in emissions.

It's always worth asking why are we hearing this now, and the significance of delaying the withdrawal of CPS until April 2028. With coal now out of the UK generation mix, the CPS brings in less and less each year to the Exchequer. Abolishing the CPS would be a relatively quick way of lowering electricity bills (albeit slightly) ahead of the next general election - which must be called by August 2029.

As Alistair McGirr, Head of Policy at SEE explains in a recent post, the removal of CPS could signal that the UK has finally reached clarity over its carbon pricing relationship with the EU. If an ETS link isn’t operational by the time CPS goes in 2028, McGirr explains, the UK economy would be exposed to the full effects of the EU's CBAM.

The announcement resulted in the price of UKAs soaring by more than 10% last week, reaching its highest level since mid-February. The market clearly buying into the story that the announcement meant the UK was making good progress in its negotiations with the EU, and that the CPS announcement was a crucial tidying up exercise ahead of establishing a link between the two carbon markets.

The broader geopolitical backdrop has added fuel to the narrative. The US/Israeli conflict with Iran has accelerated efforts to bring about a closer alignment between the UK and the EU. Prime Minister Sir Keir Starmer stated that it is in the "UK's best interest" to seek a stronger relationship with the EU, especially given the economic crisis turmoil unfolding due to the war.

To expedite the process the government are set to introduce legislation (so-called Henry VIII powers) allowing them to sign up to EU single market rules without having to consult parliament. It means that a new bill covering areas as diverse as food standards, animal welfare, linking the UK and EU emissions trading schemes, and access to the EU's internal power market could be brought forward as early as next month.

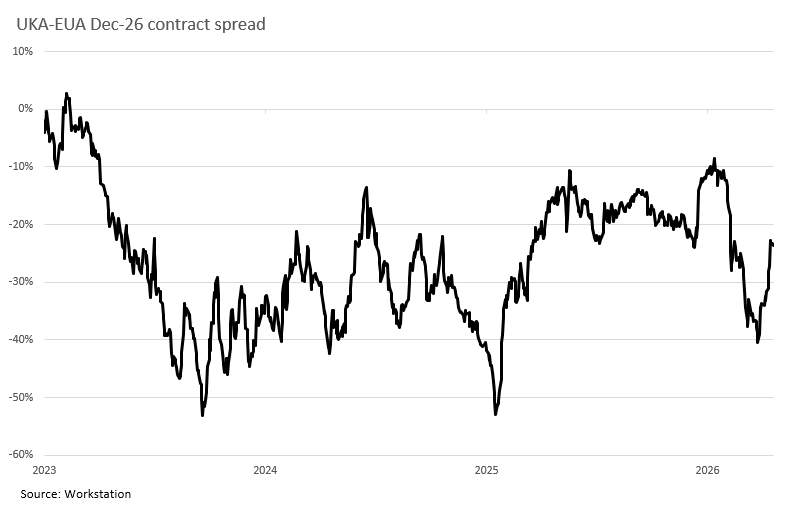

UKAs have been relatively cheap way to punt on a structurally higher EU carbon price. Recall that at one point in early 2025 UKAs were trading as low as €37.35, a 53% discount to the prevailing EUA price of €79.26. Investment funds have maintained a significant net long position (~20 million UKAs) for several months now, betting that the linkage narrative would slash the UKA discount.

While the UKA-EUA discount narrowed to around 25% in the immediate aftermath of the CPS announcement, it is still someway short of the 10% discount observed at the start of 2026. It suggests that the market senses something else is up, otherwise it really should be much closer.

The wide spread probably reflects rising UK political risk. In the short-term the risk is that Labour, the governing party, may have to elect a new leader. Longer-term, there is a strong chance that anti net zero political parties may secure power at the next general election.

Lets take a look at each in turn.

Prime Minister Starmer has come under fire for his disastrous decision to appoint Peter Mandelson to the position of US ambassador in late 2024; it was later revealed that Mandelson was a close associate of Jeffery Epstein, who he had also leaked sensitive government information to. The omnishambles relating to Mandelson's vetting is only now coming to light. The furore has led many to speculate as to whether Starmer will be forced to resign, triggering a drawn out process to elect a new leader.

Betfair's two prediction markets asking when "Keir Starmer will be replaced as Labour Leader" suggest a change is most likely to occur between July and September 2026, and very likely to be this year. At the time of writing there is an implied 70% probability that he will be gone by the end of 2026. Nevertheless, the longer he stays without being replaced, the more likely he will remain in position by the time of the next general election.

Unless Starmer resigns (or is otherwise forced out) in the next one or two months, his exit is unlikely to delay negotiations with the EU over the UK-EU ETS linkage. Furthermore, with every potential pretender to the throne likely to be more pro-EU than Starmer, the latter's exit may even accelerate the process of re-developing much closer ties with Europe – we'll come to what that might mean in a bit.

Now about Labour's competition in the polls. Both the Reform Party (currently leading in the polls and favourite to win the most seats in parliament) and the Conservative Party have promised to do away with net zero policies if they are elected, despite strong support for net zero remains in the UK. The most recent YouGov survey (carried out in December 2025) revealed a +33% net support for net zero across all UK voters. Only those who voted Reform in the 2024 general election were net opposed to net zero (-54%).

Kemi Badenoch, the leader of the opposition Conservative Party, recently pledged to "axe the carbon tax", mirroring the failed Conservative Party of Canada's campaign promise ahead of the 2025 general election. It's why securing a linkage between the UK and EU ETS is so important. Establishing a link will make it much more difficult for either party - Reform or Conservative - to break with the UK's climate targets, should they gain enough votes at the next general election (see A tactical retreat: Mark Carney axes Canada's consumer carbon tax).

A recent article by the UK political journalist Ian Dunt, argues that Labour's best strategy to outflank its political opponents is to put re-joining the EU at the centre of the next general election campaign. It would be a brave bet but with the economic damage from Brexit now clear to see, and closer ties with Europe now seen as more important than ever, the downsides are limited.

Unfortunately Starmer has squandered his political capital. Up until now the Prime Minister has chosen the path of least resistance; eking out small, politically expedient but important gains on agri-food, carbon pricing, energy trading and youth mobility. However, as Dunt explains, we are close to hitting the limits of what this strategy can achieve. The political paralysis pervading government means it is very unlikely to take this bet, unless of course, a new pro-EU leader takes over the reigns.

The price of carbon in the UK is caught in the crosshairs between two vortexes. On the one hand closer relations with the EU increase the probability that a linkage will be achieved and that UKA-EUA parity will be restored. But market participants must concede that it will come under threat as the next general election approaches.

On the other, cementing a stronger long-term link with the EU might require extreme disruption in the short-term, potentially disrupting the deal to link the two carbon markets. In the long-term though this increases the probability that the UK will remain an advocate for ambitious climate policy, with a strong carbon market at its core.

The UK introduced the CPS at a time when the EU's carbon market was stuck in its own malaise, suffocating under the weight of past policy mistakes and the eurozone debt crisis. Now today, more than a decade later, the decision to abolish CPS is a recognition that its job is done. But it's more than that. It's also a signal that the EU is the centre of gravity when it comes to climate policy, a recognition that the UK cannot achieve its climate policy aims alone, cast adrift from its nearest neighbour.