No carbon copy

Emissions trading schemes are ploughing their own furrow, and that's a risk to future growth

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

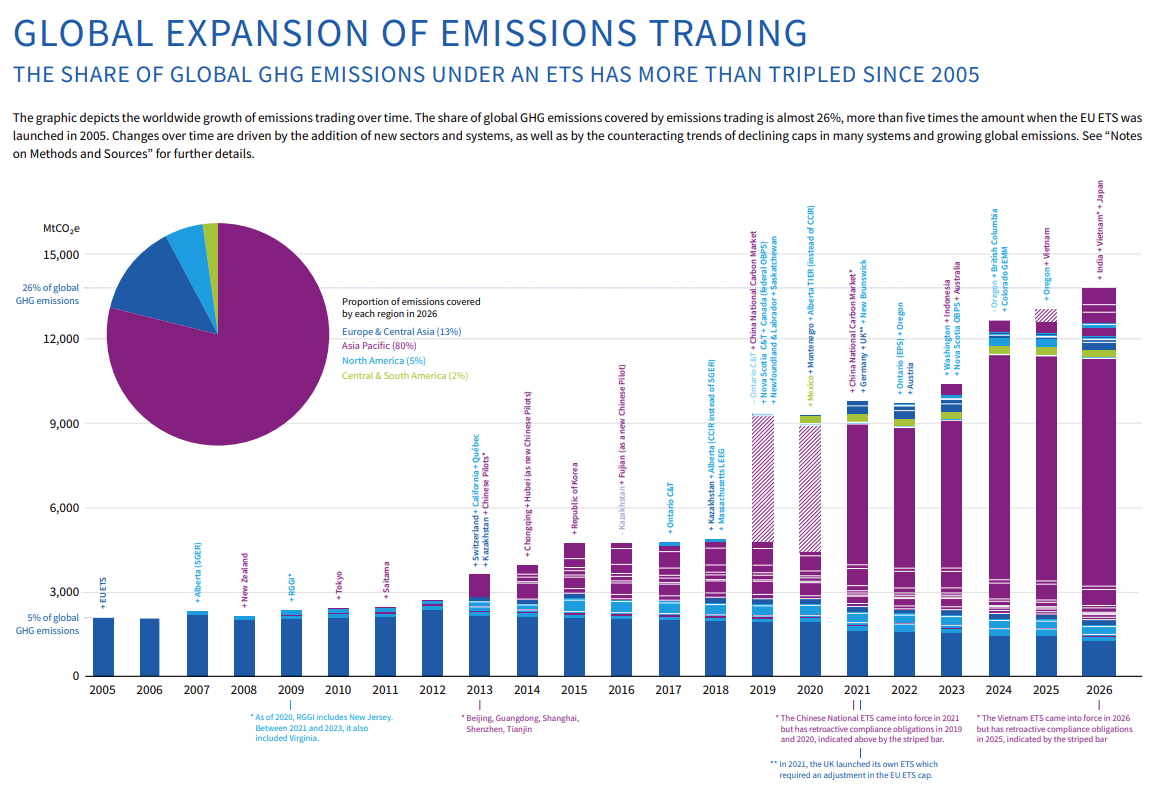

More than one-quarter (almost 26%) of global carbon emissions (equivalent to 14 Gt CO2), are covered by emissions trading systems in 2026, according to the latest ETS status report from the International Carbon Action Partnership (ICAP). Despite the adverse political environment, the share of emissions covered by an ETS climbed 3 percentage points during the past year, while the number of individual schemes increased by 3 to 41.

The share of emissions covered by ETSs has grown 5-fold since the EU ETS was launched in 2005. The EU carbon markets share of emissions has fallen over time; the decline in the overall cap offsetting the addition of other sectors, such as heavy industry, and more recently aviation and maritime.

Today, China has by far the largest ETS in terms of covered emissions (~8 Gt CO2, or 60% of the country's emissions), almost half of which has been added since 2024 as several heavy industries were added. The Chinese ETS is set to grow even further over the next few years with the inclusion of chemicals, petrochemicals, civil aviation, and papermaking.

Impetus to expand hits headwinds

Three new national-level systems (Japan, India, and Vietnam) have either launched or are due to start in 2026. Seven are currently under development and nearing operational readiness (such as Colombia, Türkiye, and New York State), while nine more are under consideration (including Bolivia, Malaysia, and Taiwan).

Asia and Latin America are the most important areas for ETS development, but the latter is the most important in terms of rising share of emissions. Just 2% of the region's emissions are currently covered by an ETS, but this is set to expand significantly, once for example, Brazil's ETS begins in the early 2030s (see Brazil's carbon market gets the green light: Policy secures the nation's climate leadership among world's biggest oil producers).

As discussed here on Carbon Risk, the launch of CBAM at the start of 2026 (the policy was first announced in 2019) has been a powerful incentive for Europe's trading partners to introduce their own carbon pricing mechanism. Analysis by Bruegel found that a 1 percentage point increase in a country’s CBAM exposure increased the probability that it would adopt a carbon pricing policy by about 2%.

Of course, these factors could start to reverse if trust in Europe's climate policy starts to ebb. Any suggestion that the EU is looking to exempt certain sectors from CBAM or weaken the compliance requirements could result in governments putting their own ETSs on the backburner. Furthermore, in the short term, current high energy prices could also cause governments to delay or cancel new ETSs, or put off expanding the coverage of existing carbon pricing mechanisms (see A green and level playing field? The European Commission faces a tortuous task refereeing CBAMs winners and losers).

Read the rest of this article with a 30-day free trial*

*and get access to the entire archive!