How to hedge long-term carbon risk

Carbon contracts for difference are the instrument of choice

A high carbon price increases the incentive for companies to invest in decarbonisation, but if the carbon price is too volatile it can actually cancel out the incentive to invest. As I discuss in The Fear Index, a 10% increase in carbon price volatility (as measured by the Carbon VIX) has the same detrimental impact on investment as a €12 per tonne decline in the carbon price.

The level of funding required to invest in decarbonising a cement plant, a petrochemical facility, or a blast furnace is enormous, requiring a multi-decade long commitment, and high sunk costs. Exposure to high carbon price volatility makes it much harder for large-scale projects to be seen as ‘bankable’ by investors

Last week the European Commission (EC) announced plans to create an Industrial Decarbonisation Bank (IDB), tasked with mobilising €100 billion over 10 years to support clean manufacturing in Europe. The main instrument the IDB will use to accelerate industrial decarbonisation is an EU-wide carbon contracts for difference (CCfD) scheme.

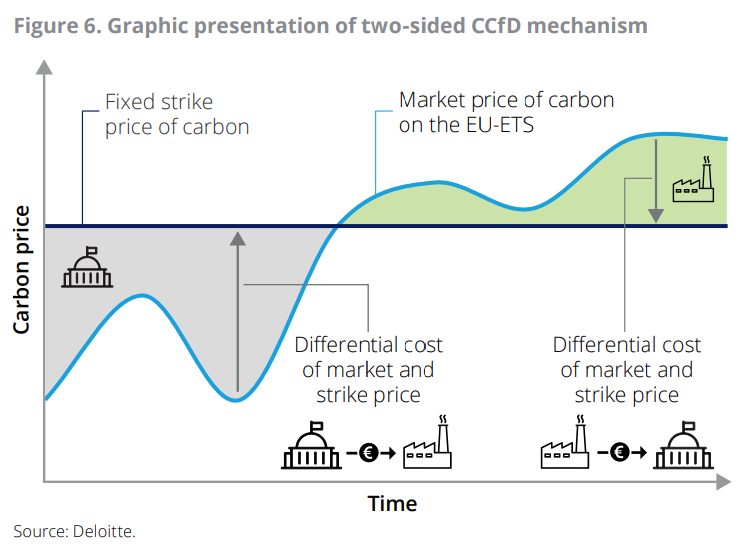

A CCfD works by setting a fixed strike price for CO2. The strike price is normally set at a level that covers the incremental capital and operating cost of the technology. It works something like this. Assume a project developer agrees on a CCfD with the EC at a strike price of €70 per tonne. If at the end of the year the average annual EUA price is €60 per tonne, the EC would pay the developer the difference (i.e. €10 per tonne).

Under a two-sided CCfD, the developer would need to compensate the government if the EUA price rises above €70 per tonne. The alternative is a one-sided CCfD whereby the developer receives a payment if the EUA price falls below the strike price, and gets to keep any excess revenues if it rises above the strike price.

At present futures contracts can only be used to hedge the EUA price up to two or maybe three years ahead. Longer-dated futures contract typically exhibit much lower levels of liquidity, hampering the ability to hedge in size. Without the ability to hedge over a longer period than this, it’s very difficult for project developers to leverage the finance necessary to fund large-scale investments in decarbonisation. CCfDs help correct for this market failure, enabling developers to put a very long-term carbon hedges in place, of around 15 years.

What factors should investors look out for in the design of the CCfD scheme?

Let’s dive in.

First, it’s important that the CCfD scheme is technology neutral. Canada’s CCfD scheme shows the danger in straying too far from this philosophy. When the Canadian government announced an initial CCfD deal in early 2024 it included an agreement on both price and volume, and involved the government taking a stake in the company concerned. In an article at the time I concluded that the Canadian CCfD scheme “fails by trying being too complex and trying to meet too many conflicting agendas.” (see Canada shows how NOT to use Carbon Contracts for Difference).

Encouragingly, the EC state that they will nurture “competitive manufacturers who drive decarbonisation through innovation, create quality jobs and contribute to our open strategic autonomy, fully respecting and applying the principle of technological neutrality for Member States as appropriate.”

Second, information asymmetries mean that it is difficult for governments to gauge the true cost of technologies necessary for decarbonisation, and the associated strike price required. For example, a new technology may come down in cost quite rapidly as industries ‘learn by doing’. A competitive bidding process such as an auction should reveal this information, making it easier for governments to set a realistic strike price.

Third, there is an argument that CCfDs could interfere in the functioning of the EU ETS. For example, it could result in less trading in the longer dated carbon futures market, damaging price discovery, and making it more costly for other market participants to hedge their risks. The risk of that occurring is probably overstated. CCfDs exist to enable hedging over periods of several years or more. The private sector does not currently offer the ability to do that, apart from isolated deals by large utilities looking to hedge the future carbon exposure of their power generation.

Furthermore, the CCfD scheme can also act as a type of commitment device, incentivising the EC to keep the price of carbon high and stable. If the EUA price were to fall significantly versus the strike price then this would represent a cost as the EC would need to recompense the project developer as part of the CCfD contract. Equally, the EC have an incentive to ensure carbon prices are broadly stable, since estimating the potential future cost that they have to bear is easier to predict and budget for.

Fourth, although a small number of EU member states have tentatively introduced CCfDs, this would be the first time that they have been employed on an EU-wide basis. In March 2024, Germany was the first country to employ CCfDs as an instrument to accelerate decarbonisation of heavy industries. In October the German government announced that 15 companies, including chemical company BASF, had been awarded support guarantees under the Klimaschutzverträge (‘climate contracts’) scheme.1

An EU-wide scheme could introduce new problems. As Deloitte outline in a recent report, while an EU-wide scheme could “enhance financial support, market integrity, cost efficiency, and foster cross-border innovation,” it may also “lack the ability to cater to country-specific needs,” while the challenge in reaching consensus among member states “could lead to prolonged implementation times.” Despite these reservations the collapse of the German government in November illustrates why an EU-wide scheme should be a net benefit. Out of the hands of individual member states, a scheme run by the EC adds to the overall credibility, increasing the likelihood that hard-to-abate industries will invest the time and resources necessary to maximise the opportunity.2

Last but not least, investors need to consider how the CCfD scheme will be funded. The EC plan to launch a €1 billion CCfD pilot scheme in 2025, with the rest of the money presumably coming into play from 2026 onwards. The EC state that it will be “based on funds in the Innovation Fund, additional revenues resulting from parts of the ETS as well as the revision of InvestEU.” LSEG are reporting that the EU ETS will account for around one-third of the total €100 billion fund and will represent “approximately 10% of the allowances auctioned from 2028 to 2037.”

There’s no suggestion that the EC will need to front-load the auction of EUAs. Recall that under REPowerEU the target was to raise €20 billion, of which less than half had been generated by the end of 2024. Even the merest hint that the EC could be looking to tap future auctions once again could prompt a sell-off in the EUA price. To do so again would only make things more difficult for the EC as they are ultimately on the hook to pay the difference versus the strike price.3

Denmark launched a CCfD scheme in 2020 in support of green hydrogen and CCS.

Almost €3 billion was earmarked for the first round of the German CCfD scheme, with the actual exposure dependant on the future price of carbon over the 15 year contract. At its launch in March 2024, Roger Habeck, Germany’s Minister for Economic Affairs and Climate Action indicated that the programme could avoid 350 Mt CO2 by 2045, with the first round of the scheme expected save 17 Mt CO2 over 15 years. ↩

https://www.deloitte.com/be/en/issues/working-together-towards-a-sustainable-future/carbon-contracts-for-difference-as-an-instrument-of-choice.html ↩

https://commission.europa.eu/document/download/9db1c5c8-9e82-467b-ab6a-905feeb4b6b0_en ↩