Pushing back on EU ETS myopia

For Europe's most influential lobby group, carbon pricing is a delicate balancing act

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

The EU's top business lobby, BusinessEurope released a report on Tuesday morning outlining its priorities for the EU ETS review. The report begins with the association stating that its members are committed to reaching climate neutrality by 2050, and that furthermore, the "ETS should remain a central part of EU’s climate policy in a post-2030 framework."

It's worth reiterating how important this stamp of approval is for the EU ETS. Described as "the Death Star of corporate lobbyists in Brussels" by the campaign group Corporate Europe Observatory, BusinessEurope represents 42 national business federations across 36 countries in the EU, the European Economic Area (EEA), the UK, and a number of other countries including Turkey and Ukraine.

In recent weeks there has been a barrage of negative comments from Europe's petrochemical producers, controversial reform ideas from Europe's climate policymakers, and even calls for suspension from some of Europe's member states (Slovakia, Czech Republic, and most recently, Italy). Now, in a welcome change, the most powerful corporate lobby group in Europe (one that can have a significant impact EU policy making) has come out in support of the EU ETS.

Nevertheless, despite their support for the EU's cornerstone climate policy, the association argues that to "ensure long-term viability", the EU must still address businesses competitiveness concerns through a range of flexibility mechanisms and strong carbon leakage measures.

Adjusting the Linear Reduction Factor (LRF) to align with 2040 targets

BusinessEurope first makes the case that the Linear Reduction Factor (LRF) post 2030 needs to be adjusted to align with the EU's 2040 targets. As currently defined, mathematically extrapolating the LRF beyond 2030 gets you to zero EUA issuance by 2039. If left untouched it would mean that in less than 15 years time a factory or a power plant would not be able to emit a single tonne of CO2 (see The zero lower bound: What happens when EU ETS emissions approach zero?).

They go on to argue that this anomaly is already preventing investment into installations with lifetimes beyond 2039. As such they call for a discussion to be initiated on how the ETS should operate beyond 2040 and 2050. Importantly, the report says that companies who have had the foresight to invest heavily in the transition should not be punished, or see their investments devalued.

Coinciding with the adjustment of the LRF, the EU should introduce additional sources of flexibility to a) preserve market liquidity as the cap edges down, b) maintain an effective price signal, recognising the innovation cycle underpinning emerging decarbonisation technologies, and c) help to maintain competitiveness amongst Europe's industries. That's quite the wish list!

Reforming of the Market Stability Reserve (MSR) to be more responsive to current economic and market conditions (e.g., liquidity issues, high carbon prices, industrial competitiveness, etc.) is one source of flexibility identified. Although they state that the MSR should retain its rules based approach in order to safeguard trust in the EU ETS, they also argue that it must "distinguish between allowances in the MSR invalidation account that are there due to emissions reductions achieved thanks to investments and innovations, from those caused by the reduction of industrial activity." That already opens up a can of worms.

Finally, recognising that industrials will never be able to get down to zero by themselves (not should they if there is a more cost effective route available), other sources of flexibility are required, including integrating technological carbon dioxide removal (CDR) into the EU ETS and international carbon credits into the broader EU climate policy architecture. As the report concludes, both options must be incorporated in such a way that they preserve the integrity of the carbon price signal and the incentive to invest in EU decarbonisation, while also improving market liquidity as we approach 2040 (see my previous articles on that subject here, here and here).

Extend free allowances and indirect cost compensation

The business association argues that even current level of free allowances and indirect carbon cost compensation are "insufficient to bridge the structural competitiveness disadvantages facing Europe."

The report argues that if CBAM does not prove effective in tackling carbon leakage by 2027 (the year an assessment is required under the CBAM regulation), then the phase-out of free allowances for CBAM sectors should be postponed. However, in contrast to calls from climate policymakers it suggests that free allowances should not conditional upon "energy efficiency measures nor preparing site level climate plans". Doing so, they argue, would be inconsistent with the technology agnostic principles underpinning the EU ETS, and "adds complexity and uncertainty without significant emission benefits." (see A green and level playing field? The European Commission faces a tortuous task refereeing CBAMs winners and losers).

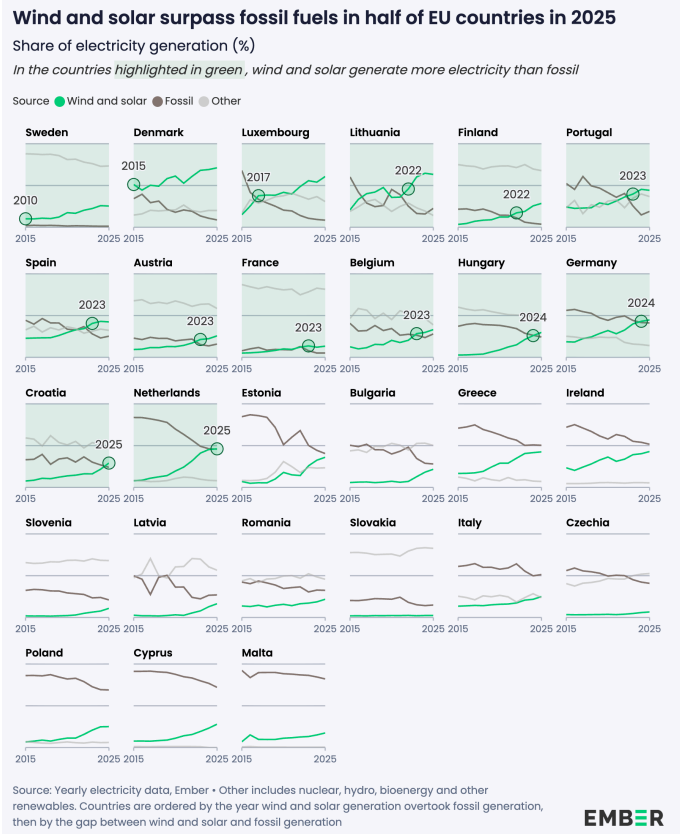

Moving on to indirect carbon cost compensation, BusinessEurope suggests that the framework should be preserved post 2030, "until a fully decarbonised energy system is achieved." It's clear that while on an aggregate level the EU is making great progress, some countries are being left behind. For example, EU wind and solar generated more electricity than fossil fuels for the first time in 2025, a situation mirrored across more than half of the EU's member states. However, its clear that many Eastern European countries as well as others Italy and Greece are falling behind.

Furthermore they argue that the list of industrial sectors eligible for compensation should be extended to "additional, currently non-covered, electro-intensive sectors where the risk of carbon leakage is high" and that more EU member states should make use of compensation. As I outlined last week, only 15 EU member states employed indirect carbon cost compensation in 2024. Meanwhile, although the Commission extended the list of industrial sectors eligible in late 2025, BusinessEurope clearly thinks this does not go far enough (see Refund policy: Industry compensation for indirect carbon costs must be conditional).

Note that the report does not make any reference to an acceptable level for the EU carbon price – the association quite clearly supports the market based approach, albeit with some safeguards. Importantly, none of their proposals, even if subsequently acted upon and implemented, will affect the market balance over the next couple of years. Nevertheless, the timing of these reports is quite informative in that they often signal when prices have moved too high (or indeed too low) and too fast.

Politicians, climate policymakers and large industrial companies were quick to point the finger at the need to reform the EU ETS when carbon breached €90 in mid-January. The subsequent publication of this report, and especially BusinessEurope's explicit support for the EU ETS, is perhaps a signal that the EU carbon price may now have fallen too far.