Electric avenue

Europe set to outline its path to electrification and energy security

After four years of brutal conflict between Russia and Ukraine right on its doorstep, you would think that Europe would be aware of the risks of being too reliant on fossil fuels.

True the bloc has largely diversified away from Russian natural gas and ramped up its renewable capacity, but fossil fuels still account for almost 60% of Europe's final energy consumption. The vast majority of the oil, gas and coal is consumed outside the power sector: to fuel transportation, used in industrial processes, and to heat buildings.

That dependence is even more acute because of the blocs reliance on energy imports. Almost two-thirds of its primary energy supply arrives from outside the EU. The only other major economies to have a higher fossil fuel import dependency are Japan (84%) and South Korea (80%).

It appears that many governments became complacent about the potential economic risks, and in particular, the damage that can be caused from energy price shocks.

For example, Italy is one of the countries most exposed to the energy price shock emanating out of the Gulf. Sourcing 36% of its LNG imports from Qatar, and with natural gas setting the price of electricity almost 90% of the time, Italy is particularly vulnerable.

Instead of tackling the source of its angst, the Italian government has sought to deflect the blame, calling for the EU ETS to be suspended.

Powering up Europe's energy security

Electrification is central to improving Europe's energy security and competitiveness, enabling it to diversify its energy sources while also improving overall energy productivity - the amount of GDP produced per unit of energy.

As the Carlyle Group outline in a recent report, electrification enables different fuels to "compete to supply joules through an increasingly connected grid," with the optimal mix dependent "not just on what is available to a country, but also on what it can provide."

Carlyle note that nuclear power has high upfront capital costs and long lead times, but it provides stable and inexpensive power. European Commission President Ursula von der Leyen recently admitted that it was a "strategic mistake for Europe to turn its back on a reliable, affordable source of low-emissions power."

The private equity firm notes that renewables plus battery storage has a high upfront capital cost and is relatively quick to deploy. Once established the marginal cost of renewables is low, but generation suffers from intermittency. Europe has succeeded in expanding its renewable energy capacity by around two-thirds since 2021, to the point that in 2025, solar, wind and hydro generated almost half (48%) of the EU's electricity (see Europe's new joule order).

Finally, fossil fuels can deliver dispatchable power (ensuring price and grid stability), albeit it with a higher marginal costs and a marked vulnerability to trade disruptions. Despite calls from some quarters to increase domestic production, Europe has never been a significant producer, and even with significant investment it will still be highly dependent on imported fossil fuels, and the price volatility associated with that.

To maximise more of what its got available to it, and what it can provide, Europe must increase its electrification rate.

Unfortunately for Europe, electrification (measured as a share of electricity in final energy consumption) has stagnated at around 23% for the last 15 years. Although its performance is only slightly better than the US, both economies have been overtaken by China. Over the past decade the latter's electrification rate has steadily increased. Overtaking Europe and the US in 2016, it now stands at almost 30%.

Even within Europe, not all member states are at the same level. For example, Sweden has an electrification rate of around 33%, while Romania is closer to 15%. It also varies significantly even in the same sector; 18% for Slovakian iron and steel producers compared to 57% for furnaces located in France. Nevertheless, the wide disparity, whether by household or by sector, shows that gains in electrification can be made.

It's not for want of the right technology, much of which is already commercially available.

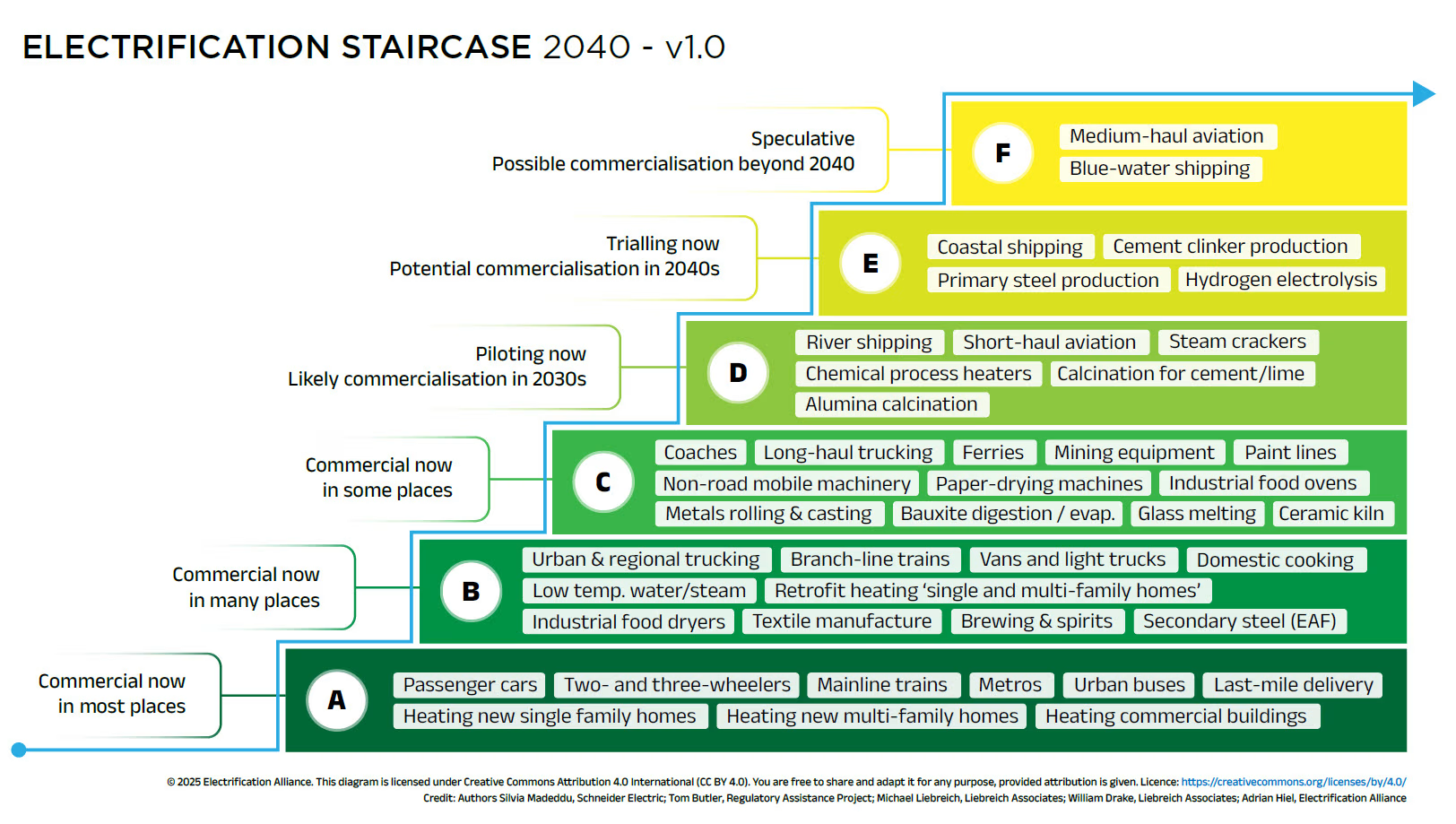

Climbing the 'Electrification Staircase'

The 'Electrification Staircase' was developed by the Electrification Alliance, a coalition of industry groups and NGOs calling for electricity to be recognised as "the key energy carrier for an efficient and decarbonised European future."

Inspired by the 'Hydrogen Ladder' developed by Michael Liebreich, the Electrification Staircase illustrates where electrification can deliver the highest impact today, helping policymakers, regulators and industry to make informed choices on the sequencing of electrification.

Steps A, B and C include examples of electrification that are commercial viable now, at least in some places. Most of the examples relate to transportation and heating, but they increasingly include industrial applications such as textile and paper drying machines, steel manufacture using secondary steel, and mining equipment (see Heat pumps on the factory floor).

Moving further up the staircase (steps D, E and F) you get to more speculative options that are not at the stage where they are being widely commercialised. For example, coastal and river shipping, short-medium distance aviation, and industrial processes (electrolysis, calcination, etc).

If the technology is available then, why has Europe's electrification rate stagnated?

First, the cost of electricity is between two and five times higher in Europe than in China or the US. While some countries, Spain for example, are now in a position to benefit from renewables low marginal cost, others are much more dependent on higher cost, more volatile natural gas to set power prices. Second, a fragmented energy market means investment and operational decisions are split across member states, leading to delays to investment and higher costs. Finally, there is no clear strategy as to how electrification should be prioritised across the European economy. It leaves individual member states to come up with their own plans, ultimately failing to maximise the benefits from coordination.

All of these factors are interrelated of course, which is why reform is overdue

Sparking up a plan of action

To that end the Commission has been consulting on an Electrification Action Plan (EAP) aimed at stimulating electrification in sectors covered by the Renewable Energy Directive (RED III), specifically transport, space heating & cooling, and industrial applications. The EAP is currently scheduled for adoption in the second quarter of 2026. So what did European industry chiefs think were the priority areas for reform?

According to energy technology multi-national Schneider Electric, the Commission needs to put in place measures that accelerate upgrading Europe’s electricity grid, so that it can accommodate more renewable power and meet rising demand for electricity. Reform taxation to create a level playing field with fossil fuels (i.e., cutting taxes and levies on electricity, switching them to gas or general taxation instead) and by facilitating access to stable, long-term power price contracts. Lastly, focus on the most mature electrification opportunities and prioritising applications where adoption can lower operational costs and ensure fast reductions in emissions.

Other proposals put forward by energy intensive industries tend to focus on short-term measures that alleviate or otherwise protect heavy industry from being undercut by competition from lower-energy cost jurisdictions. For example, the Alliance of Energy Intensive Industries has said that the EAP should enhance indirect carbon price compensation, shield energy intensive companies from total system costs related to grid upgrades, stating that the EAP will ultimately only be judged a success if it brings industrial electricity costs closer to €50 per MWh (see Refund policy: Industry compensation for indirect carbon costs must be conditional).

Under the Clean Industrial Deal, Europe has an indicative electrification target of 32% by 2030. It is highly unlikely to be achieved given the lacklustre progress made to date. In the absence of a major policy change, Strategic Perspectives, a pan-European climate think tank, is projecting that electrification could hit 39% by 2040 under its business-as-usual scenario.

In order to really brake the stranglehold that fossil fuel import dependency has on Europe the EAP really must move things along much faster. The analysts at Strategic Perspectives argue that "electrifying half of the European economy by 2040 is the best strategy for its international competitiveness and energy security."

Although the EU would need to invest an additional €55 billion per year in the grid and clean technology versus business-as-usual, it would result in annual savings of €43 billion in fossil fuel imports and €41 billion in carbon costs, leaving Europe a net €29 billion per year better off.

Chicken and egg

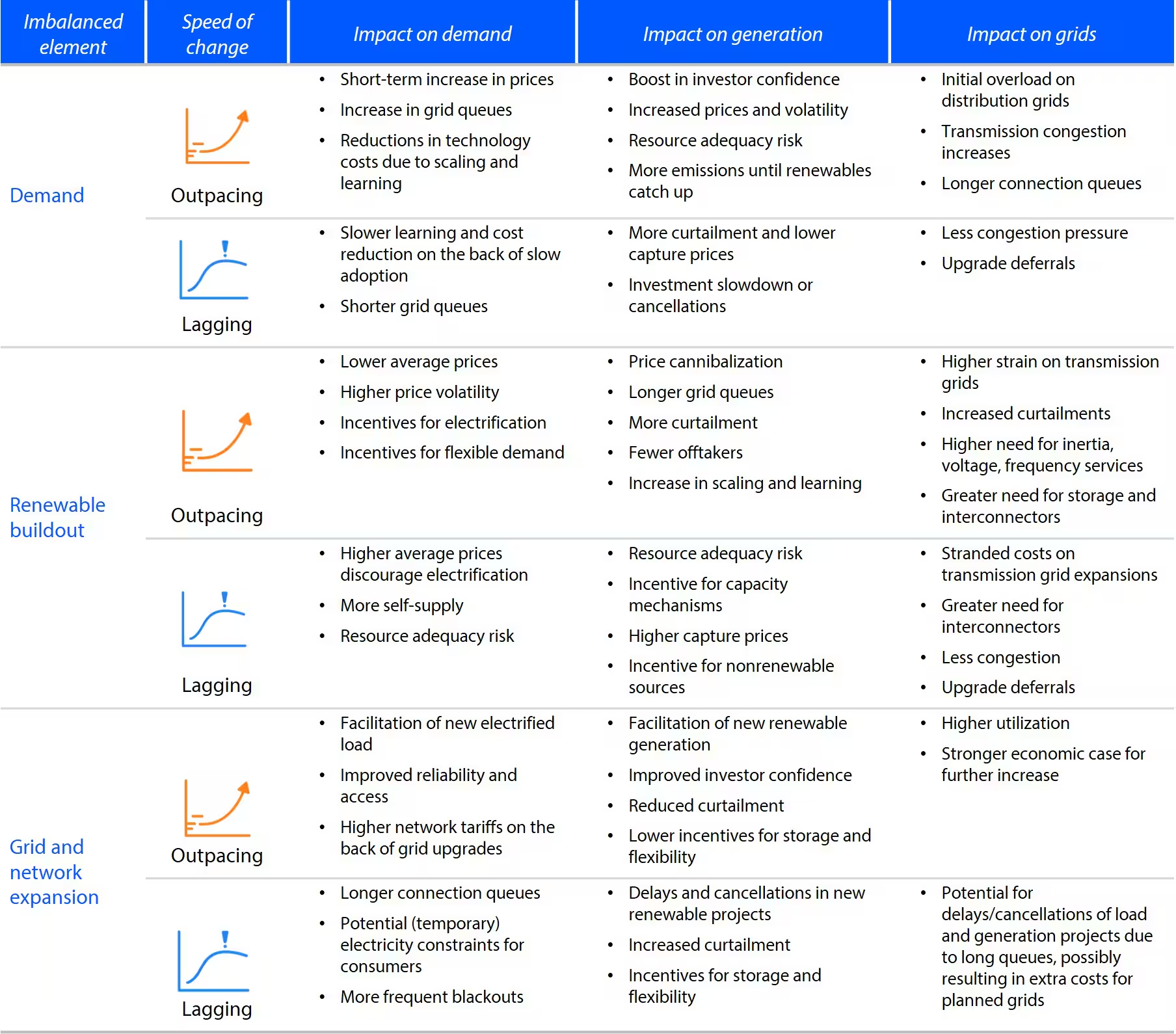

Fossil fuel shocks will not disappear any time soon, but as their share of final energy consumption declines over time, price volatility will affect the economy to a progressively lesser extent. But as Peter Garnry of Gasda Capital cautions in a recent article, as the economy becomes increasingly electrified, power shocks will emerge as a new threat.

"Because electricity is not traded globally, power shocks will be more regionally contained, which is a good thing. However, as electrification increases, our electricity intensity (electricity needed for GDP growth) will likely rise, and disruptions will begin to hurt across data centers, transportation, heating, and other critical sectors. So while oil shocks will diminish in impact, the future is likely to hold power shocks instead."

Part of the reason for this is that electrification involves solving a classic chicken-and egg problem. Electricity demand growth, installing additional power generation capacity, and upgrading the grid is highly interdependent. Electrification is a dynamic process in which any element deviating from the ideal risks tripping up the entire system. As the table from Rabobank below illustrates, price volatility is one of the potential knock-on impacts.

There is no diversification without electrification, but as Lucy Shaw at the Slow Burn newsletter notes, electrification by itself is not a sufficient condition for energy security, unless domestic generation is also secure. For example, China has paired fossil fuels with electrification, building thermal coal generation plants and burning its own huge domestic reserves of coal when renewable energy generation isn't able to meet demand and balance the grid.

Europe now needs to find its way forward to energy security, competitive energy prices, and a decarbonised economy. Solving the chicken and egg problem will probably mean some element of fossil fuel generation is required. Far better to extract those fuels domestically in as low carbon a way possible, free from foreign interference.

The conversation of how Europe moves forward to an electrified economy is long overdue.

MUSCIAL CODA

"Rock down to Electric Avenue" by Eddy Grant refers to a market street in Brixton, London, earning its name in 1888 to be the first lit by electricity in the UK.