Repost: Spread bets

Why "energy transition assets" could drive commodity trading returns

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

I'm travelling this week and so in a break from the normal schedule I thought I'd share an article from the Carbon Risk archive.

I'm lifting the paywall on an article I originally published in March 2025 in which I discuss the outlook for low-carbon commodities and "energy transition assets". It's a topic that I believe will become increasingly relevant as trading firms, governments, and large industrial companies realise the value in market-based mechanisms that can drive decarbonisation.

Stuck for something else to read? Check out the rest of the Carbon Risk archive (451 articles). Normal service will resume after Easter.

“The commodity traders are arbitragers par excellence, trying to exploit a series of differences in prices…They are, in the words of one academic, the visible manifestation of Adam Smith’s invisible hand.”

- Javier Blas, The World for Sale: Money, Power, and the Traders Who Barter the Earth's Resources

Commodity trading profits slumped from $100 billion during 2022 and 2023 to $72 billion in 2024, according to preliminary estimates by McKinsey. A return to a more ‘normal’ trading environment, characterised by lower and less volatile energy prices and fewer geopolitical disruptions, has dampened margins.

The adverse impact was greatest for those traders covering oil & oil products, and power & gas. The total margin generated across these two commodity sectors, which together normally account for two-thirds of the total, declined by almost 40% versus the period 2022/23.

The boom years marked by Russia’s invasion of Ukraine attracted new entrants into the market and incentivised existing firms to expand their operations. As uncertainty and price volatility has subsided, so the increase in competition has also acted to reduce the margins available.

The world for sale

Of course, commodity trading firms do sometimes take directional bets on the price of various commodities, but it would be incorrect to suggest that is their primary purpose. Commodity traders play an essential role in the global economy, ensuring that the resources we need on a daily basis - energy, raw materials, and food - are there when we need them.

A small number of huge commodity trading firms dominate the production, transportation and trading of commodities. Virtually all commodities must undergo a variety of processes to transform them into things that we can actually consume. These transformations can be grouped into the following categories: space, time and form.

The first transformation requires the transportation of commodities from where they are produced to the places they are consumed. The areas where commodities can be efficiently produced, such as fertile land or mineral deposits, are usually away from, and often far away from, where those who desire to consume them reside.

The second transformation requires commodities to be stored to correct for mismatches in the timing of production and consumption. Stocks can be accumulated when supply is unusually high or demand is unusually low, and can then be drawn down upon when demand exceeds supply.

Finally, commodities must often undergo transformations in form in order to be suitable for final consumption or for use as an input in a process further down the value chain. For example, crude oil must be refined into gasoline, diesel and other products.

Commodity trading firms seek to identify the most valuable of these transformations, undertake the transactions necessary to make these transformations and engage in the physical and operational actions necessary to carry them out (see Know your onions: Concern over the role of speculators in Europe's energy markets is overplayed).

Right now, the returns from these transformations are under pressure, but that’s not expected to last long. Taking a longer-term view, McKinsey are forecasting a return to a steady margin growth (~10% per annum) with overall industry profit expected to return to $100 billion before the end of the decade.

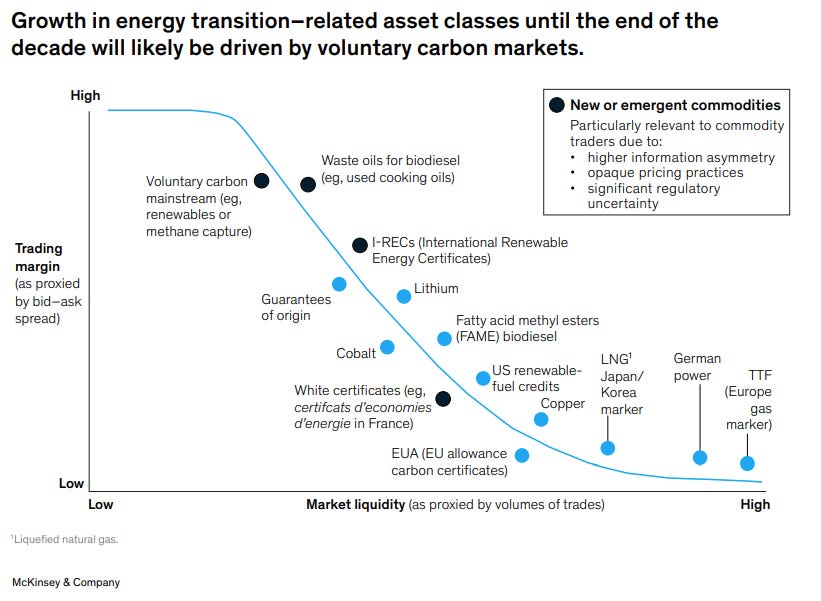

Power, gas, and LNG markets are likely to drive much of the increase, supported by market liberalisation, the growth in electricity demand (+3.5% per annum), and weather related volatility as renewable adoption rises. McKinsey also expects “energy transition assets”, such as carbon credits, biofuels, energy attribute certificates (EACs), and green premium certificates (GPCs) to be a major source of growth.

Let’s take a look at the opportunity for commodity traders across each of the four markets.

1. Carbon Credits

Although McKinsey acknowledges that forecasting carbon credit volumes and prices “remains a highly uncertain exercise,” they point to three factors that are likely to drive growth for commodity trading firms. First, acceptance of carbon credits by compliance markets, driving up the pricing of eligible credits. Second, demand from the aviation industry as CORSIA reaches full implementation. Third, demand for credits from corporations looking to meet 2030 net-zero targets.

As I outlined in Coming of age: The evolution of carbon credits fits a pattern of financial innovation, COP29 marked a significant milestone in the advancement of international carbon credit trading. Banks and other financial institutions that had stepped back from the carbon credit market, or had until recently decided not to establish a trading desk are likely to want to get back in. One of the key obstacles that is now on its way to being resolved is the question of trust:

“Over 35 years ago, carbon credits emerged as a tool for companies to reduce their impact on the climate, in the absence of any regulation requiring them to do so. Almost 20 years ago, the first framework for international trading in carbon credits was developed. But those early pioneers, hoping this would catalyse global carbon markets into action, would be left disappointed.

And then, borne out of the ashes of the 2012 carbon panic, the VCM stepped into the void. It too experienced its own boom and bust as the unregulated marketplace came under fire. Now, according to Hannah Hauman, global head of carbon trading at Trafigura, agreement on Article 6 means that carbon credits are set to join the ranks of “investment-grade assets and operations.”

The carbon credit market is coming of age.”

2. Biofuels

McKinsey also expects biodiesel to be a major source of margin growth for commodity traders. The opportunity is driven by European regulation (e.g., RED III, EU ETS2, SAF mandates) and uncertainty over the the US governments position, particularly around SAF production support.

In 2023 the EU adopted an amendment to the Renewable Energy Directive (RED III) that raised the collective target for renewables in transportation from 14% to 29% by 2030. At the same time it introduced a parallel target to reduce the carbon intensity of 14.5% of transport fuels. Meanwhile, the launch of ETS2 in 2027 is expected to see an increase in demand for biofuels to reduce the exposure to carbon pricing by the transportation sector.

The ReFuelEU aviation mandate requires EU airports and fuel suppliers to increase the share of aviation fuel that includes SAF from at least 2% in 2025, to 6% in 2030, with the percentages then ramping up every five years to 32% in 2040, before hitting 70% in 2050. Meanwhile, the UK Government published its SAF mandate in early 2024, and at least in the near term its more ambitious than the EU. Set at 2% in 2025 the share of aviation fuel from SAF will need to rise to 10% in 2030 and then 22% in 2040.

America’s targets were arguably more ambitious than Europe’s. In contrast to the mandate approach in Europe, the U.S. depended on giving fuel producers tax credits that partially cover the cost difference versus kerosene. SAF producers were eligible for a tax credit of up to $1.25 per gallon under the Inflation Reduction Act (IRA), but that tax credit program expired at the end of 2024.

However, Donald Trumps hostility to climate initiatives has sowed doubt over the future support for SAF after he paused clean energy funding. The process to finalise the SAF regulations is currently on hold, in accordance with the 60 day freeze on all regulatory developments put in place after Trump was inaugurated.

Europe has favoured so-called second generation biofuels including agricultural and forest residues, and waste products such as used cooking oil (UCO) and animal fats to meet its renewable fuel targets. Biofuels derived from these waste products are commonly referred to as Hydro-processed Esters and Fatty Acids, or HEFA. However, doubts have surfaced as to whether the supply of UCO is really sustainable, with concerns that Chinese suppliers have blended virgin palm oil with UCO (see Frequent fryer: Demand for biofuels made from used cooking oil is soaring, but could there be a sting in the tail?).

3. Energy Attribute Certificates (EACs)

The third major opportunity for margin growth is expected to come from Energy Attribute Certificates (EACs). Known as Guarantees of Origin (GOs) in Europe, or Renewable Energy Certificates (RECs) in North America, EACs document that one MWh of electricity has been generated and supplied (net) to the grid, through a specified renewable energy resource.

EACs are based on a “book and claim” chain of custody market mechanism. They enable suppliers of low-carbon solutions to “book” the environmental attributes of a good they have produced (power generated via renewables, emission savings, etc), and for users to “claim” those same attributes.

EACs can be very volatile due to political and weather related factors. For example, a drop in hydropower output in Europe during 2022 resulted in GO prices spiking 10-fold to around €10 per MWh. A couple years later prices had collapsed due to an increase in renewable energy generation and weaker power demand. The UK’s decision to exit from the EU and the Norwegian governments threat to pull out of the GO market both caused a spike in GO price volatility due to their position in the market - the UK a net importer, Norway a net exporter.

McKinsey notes that “these markets are expected to remain highly valuable, with forward curves suggesting sustained elevated pricing of existing products and new international markets emerging, as evidenced by China’s recent launch of a domestic replacement for RECs”. Indeed, the introduction of mandatory emissions reporting - in Europe and elsewhere - was expected to increase demand, but political decision to delay or soften obligations on businesses could change that (see Book and claim - Part 1: Energy Attribute Certificates play a vital but controversial role in the energy transition,

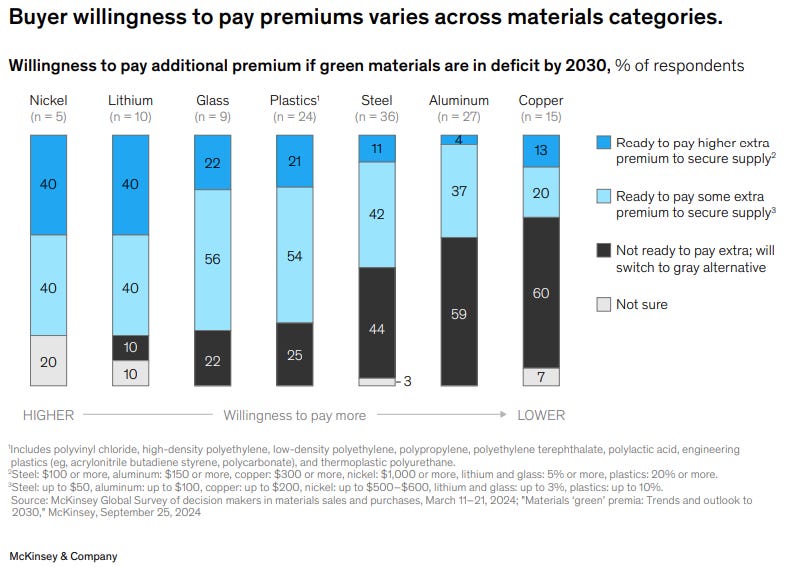

4. Green Premium Certificates (GPCs)

Finally, McKinsey sees the growth of Green Premium Certificates (GPCs) as an opportunity for growth. Although the consultancy refers to demand from the metals sector (given their role in the energy transition), their potential extends well beyond and includes nascent commodities such as Sustainable Aviation Fuel (SAF) and green hydrogen (gH2).

GPCs are instruments that represent the emissions attributes, and emission relate claims, after using a metric tonne of a low carbon fuel or other commodity. They have similar characteristics to the EACs as they unbundle the environmental attributes from the underlying commodity, enabling buyers to pay for the environmental benefits, even if the physical commodity is not yet available for them to use (see Book and claim - Part 2: How SAF and green H2 are harnessing the power of Energy Attribute Certificates).

A McKinsey survey of shows growing willingness to pay for green premiums across several materials, including lithium and nickel. Commodity research firm CRU defines the green premium as: “An additional price, over and above that paid for the equivalent ‘standard emissions’ substitute, that the consumer or buyer will pay due to the lower CO2e emissions associated with a product.”

A separate report by Oliver Wyman suggests that low-carbon commodities could dominate commodity trading returns. The consulting firm projects that their share of total margins could rise from 16% in 2022 to 26% by 2030, and then surge to 65% in the long-term as we approach 2050. GPC’s are likely to be an important addition to the global commodity trading framework, enabling buyers and sellers to trade the green premium without taking physical delivery.

As McKinsey notes, one of the most important similarities across carbon credits, biofuels, EACs, and GPCs is that participation “requires adherence to stringent regulatory criteria along with a robust documentation system to ensure traceability of commodities traded.” Given their expertise in trading commodities across various jurisdiction, commodity traders are in a strong position to leverage their capabilities to drive growth in “energy transition assets”.

As commodity traders returns have come under pressure recently, the future looks very promising indeed. The power super-cycle and the knock-on impact on natural gas, LNG trade, and compliance carbon markets is the background to the next decade. Layered on top of that though, the emergence of carbon, biofuel, EACs, and GPCs is likely to offer a host of opportunities for commodity traders.

I’ll leave the last word to Javier Blas, author of the excellent book ‘World for Sale’, “as long as markets are less than perfectly efficient, there will still be money to be made - even without walking the knife-edge between legal and illegal - by exploiting inefficiencies and moving commodities around the world in response to price signals from the markets.”