Greener growing still in the red

From the Strait of Hormuz to Hauts-de-France, Europe's response to the fertiliser crisis must tackle 'green' profitability

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭.

Roughly one-third of global fertiliser trade (primarily ammonia and urea) passes through the Strait of Hormuz, along with 20% of liquified natural gas (LNG) and 45% of sulphur, the latter both key raw materials in the manufacture of synthetic fertiliser.

Europe receives only a negligible amount of its fertiliser needs from the Middle East. Other countries, most notably India, Pakistan, Australia and New Zealand, are much more exposed, receiving 25-30% of the fertiliser they consume from the region.

Nevertheless, the EU is still one of the most fertiliser-dependent agricultural regions in the world. The bloc imports enough fertiliser to meet more than 60% of its needs; although for some types (such as potash and phosphorus) that dependence is closer to 100%.

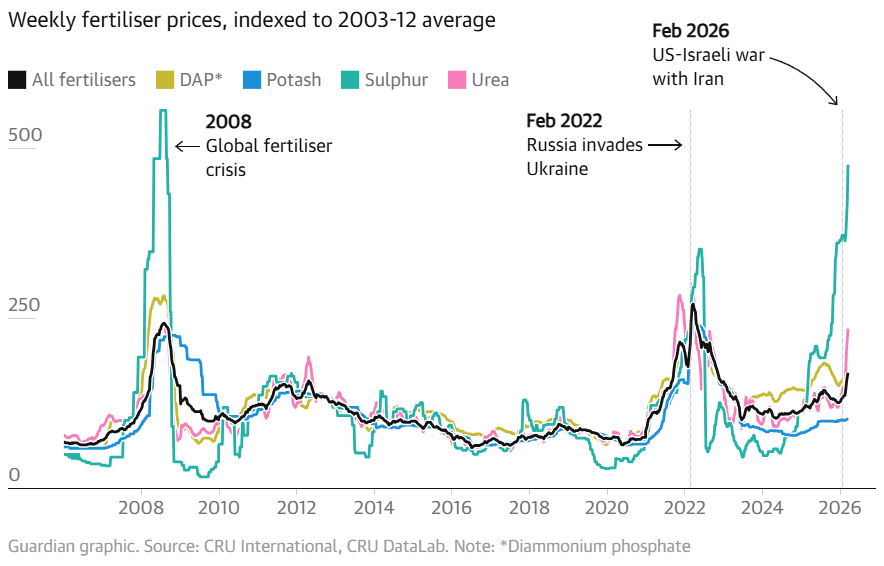

As with oil and gas, the price of other commodities, including ammonia and urea, are set on global markets. And here Europe is also a price taker. Iran's chokehold on shipments through the strait has lifted the price of fertiliser, but so far at least, not to the same extent as either 2008 or 2022.

For now, countries are content to wait (nervously), and hope volumes normalise, whether a ceasefire holds or not. There's no scramble for product, not yet!

The crisis could not have come at a more difficult time for Europe with farmers already smarting at the additional (albeit negligible) cost of fertiliser due to the introduction of the Carbon Border Adjustment Mechanism (CBAM) at the start of 2026. The policy means that importers of several carbon intensive products, including fertiliser must now factor in the cost of the embedded emissions in the product they bring into the EU.

Europe imported more than a quarter (28%) of its annual demand for nitrogen-based fertilisers in December alone. What now might be seen as an amazing stroke of luck was actually a quirk of timing, as importers sought to avoid the regulatory burden. Could CBAM or an alternative climate policy offer a way out for Europe from its impending fertiliser crisis? Let's hold our noses and brave the pungent air of what may be the path towards a greener and less insecure dependence on fertiliser.

Read the rest of this article with a 30-day free trial*

*and get access to the entire archive!